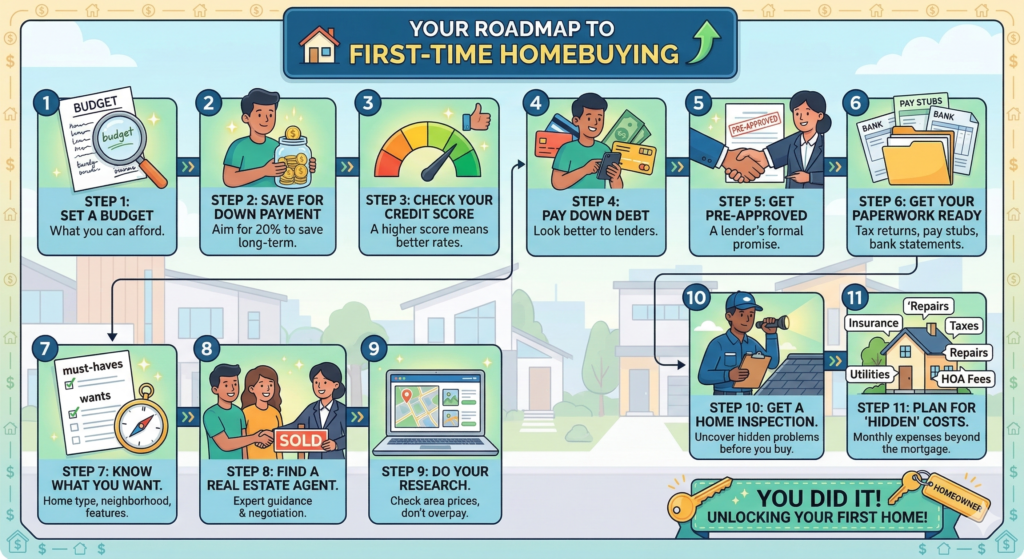

1. Set a Budget

Before you look at houses, decide how much you can actually afford to pay each month. Remember to think about what a bank will let you borrow versus what you feel comfortable paying.

2. Save for a Down Payment

Try to save 20% of the home’s price if you can. This gives you a head start on owning the home, helps you avoid extra insurance costs, and keeps your monthly payments lower.

3. Check Your Credit Score

Lenders look at this number to decide if they will give you a loan and what your interest rate will be. A higher score usually means a better deal.

4. Pay Down Debt

Cleaning up your current debts (like car loans or credit cards) makes you look better to lenders and helps improve your credit score.

5. Get “Pre-Approved”

Talk to a lender to find out exactly how much they are willing to lend you. A pre-approval is better than a “pre-qualification” because it uses your real financial documents to prove you are a serious buyer.

6. Get Your Paperwork Ready

Lenders will need to see several documents, including:

- Your ID and Social Security number.

- The last two years of tax returns and W-2s.

- Your last 30 days of pay stubs.

- Your last two months of bank statements.

7. Know What You Want

Make a list of “must-haves.” Ask yourself:

- How long do I plan to live there?

- Do I want a house, a condo, or a townhome?

- What neighborhood do I like?

- Am I okay with a “fixer-upper,” or do I want it move-in ready?

8. Find a Good Real Estate Agent

Ask friends or family for recommendations. A good agent will guide you through the search and handle the tough negotiations.

9. Do Your Research

Look at what other homes in the area have sold for recently. This helps you make a fair offer so you don’t overpay.

10. Get a Home Inspection

Once you find a house you love, hire a professional to check it for problems. Make sure your offer says that you can back out if the inspection finds major issues.

11. Plan for “Hidden” Costs

Owning a home costs more than just the mortgage. Make sure your monthly budget includes:

- Homeowners insurance and property taxes.

- Utilities (electricity, water, trash).

- Repairs and lawn care.

- Homeowner Association (HOA) fees, if applicable.