Mastering Your Credit Score

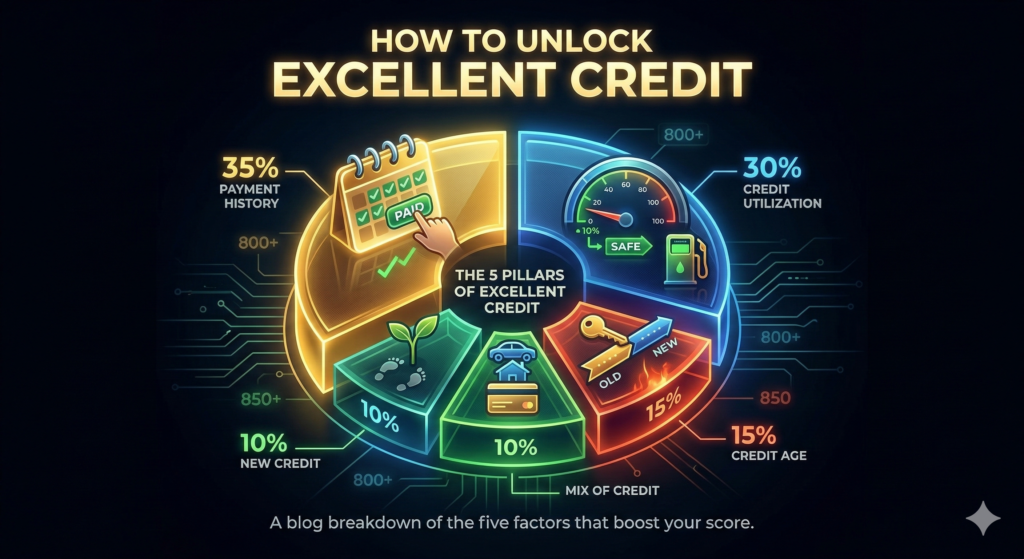

Achieving an “excellent” credit score (typically 800 or above) isn’t about magic tricks; it’s about mastering five specific behaviors that credit bureaus track. Because you asked for detail, here is a breakdown of the “Credit Score Pie” using simple language and analogies to show how each piece works.

1. Payment History (35% – The “Foundation”)

This is the single most important factor. Lenders want to see that you are a person of your word. Every time you pay a bill on time, you are essentially telling the bank, “I am reliable.”

Analogy: Think of this like your GPA in school. Getting an ‘A’ on a test (making an on-time payment) keeps your average high. However, failing one major exam (a late payment) can tank your entire average, and it takes a long time to pull it back up.

Pro Tip: Even being 30 days late just once can drop an excellent score by 100 points. Set up “Autopay” for at least the minimum amount to ensure you never miss a date.

2. Credit Utilization (30% – The “Safety Margin”)

This looks at how much of your total credit limit you are actually using. If you have a $10,000 limit and you owe $9,000, you look “maxed out” and risky.

Analogy: Imagine a gas tank. If you are constantly driving with the needle on “Empty,” you’re at high risk of being stranded. Lenders prefer to see you driving with a full tank but only using a tiny bit of gas—it shows you have plenty of “fuel” (money) and aren’t desperate.

The Rule: Aim to keep your balance below 10% for an excellent score. While many say 30% is okay, those with the highest scores usually stay in the single digits.

3. Length of Credit History (15% – The “Experience Factor”)

Credit bureaus want to see how you handle money over a long period. They look at the age of your oldest account, your newest account, and the average age of everything in between.

Analogy: Think of this as a Job Resume. A teenager with a 4.0 GPA is great, but a professional with 20 years of consistent “A” performance is more trustworthy.

The Rule: Never close your oldest credit card, even if you don’t use it. Closing it “erases” part of your history and makes your credit profile look “younger” and less experienced.

4. Credit Mix (10% – The “Versatility Factor”)

Excellent credit holders usually have a mix of different types of debt, such as “revolving” credit (credit cards) and “installment” loans (car loans, mortgages, or student loans).

Analogy: This is like being a “Well-Rounded” Athlete. If you can only play one sport (credit cards), you’re okay. But if you can play baseball, basketball, and soccer (different types of loans), it shows you have better overall coordination and can handle different rules and schedules.

5. New Credit (10% – The “Desperation Check”)

Every time you apply for a loan or a new credit card, a “hard inquiry” is recorded. Opening too many accounts in a short time makes you look like you’re in a financial crisis.

Analogy: If you walk into five different banks in one afternoon asking for money, they’re going to wonder, “Why do you need so much cash all of a sudden?”

The Rule: Space out your applications. Only apply for new credit when you truly need it.

Summary of the “Excellent” Habit List:

If you want to move from “Good” to “Excellent,” follow this checklist:

- Never miss a payment (use Autopay).

- Keep balances very low (under 10% of your limit).

- Don’t close old accounts (keep the history alive).

- Check your report for errors (mistakes by banks can lower your score).

- Be patient (Time is the one factor you can’t rush).